When it comes to saving, we are not all equal. However, sometimes it only takes a little to build one and strengthen it regularly. A look back at 3 simple and effective methods to put aside each month without deprivation, even on a tight budget.

Source : Christian Dubovan via Unsplash

Source : Christian Dubovan via Unsplash

Rising bills, sometimes difficult monthly ends and low interest rates do not encourage the French to save. Fortunately, some budgeting methods have proven themselves and allow you to set aside funds regularly and sustainably.

Here are three surprising approaches, both simple to implement and suitable for all profiles. Their promise: to be able to generate significant precautionary savings, without having to sacrifice the essentials, just by focusing on your budget for a few minutes per month. Explanations.

The 50-30-20 method: quick, effective, but to be adapted according to the budget

To save each month without having to enter into apothecary calculations, the 50-30-20 method has largely proven itself. Concretely, this approach draws its effectiveness from a good distribution of expenses.

According to this method, on average 50% of revenue must be devoted to irreducible costs. Rent, credits, taxes, insurance, mutual insurance and generally all expenses that the household cannot escape are recorded in this category.

And you, what proportion of your income can you dedicate to your savings? // Source: Niko Nieminen via Unsplash

And you, what proportion of your income can you dedicate to your savings? // Source: Niko Nieminen via Unsplash

30% of resources are attributable to all other expenses, those which can be more or less adjusted over time by making competition work. This concerns both food shopping, electricity or gas bills, as well as your leisure and pleasure purchases.

THE Remaining 20% of your income are then dedicated to savings.

To illustrate this method, based on a net salary of 2,000 euros per month:

1,000 euros is used to pay for your accommodation, taxes and essential bills; 600 euros are reserved for your food, but also for your various purchases, travel and leisure activities; 400 euros can then be placed in a savings account.

Such a budget distribution is a benchmark for a middle-class household. It must therefore be reviewed and adapted to your situation. A person with a high level of income, but with a rather modest lifestyle, can in fact increase the portion dedicated to their savings.

Conversely, if you are from Ile-de-France and have to make it through the month on a minimum wage, it is likely that 20% savings is far too restrictive, if not impossible, to follow. Behind this approach, the idea is absolutely not to deprive yourself of eating, for example, but to find the right balance between irreducible burdens and pleasure.

Moreover, for the tightest budgets, other methods are clearly more suitable than 50-30-20. Here they are.

The Kakeibo method (pronounced “kakébo”): the most fun

This is an approach that has stood the test of time. Developed in 1904 by Hani Motoko, a Japanese journalist who wanted to help women keep household accounts, the Kakeibo method is intended to be simple and fun. Better still, it is applicable to everyone, from the most modest to the most well-off.

Get out your notebook, pen and calculator (or an Excel spreadsheet), prepare your latest bank statements, and quickly warm up your wrist. The day of reckoning has come !

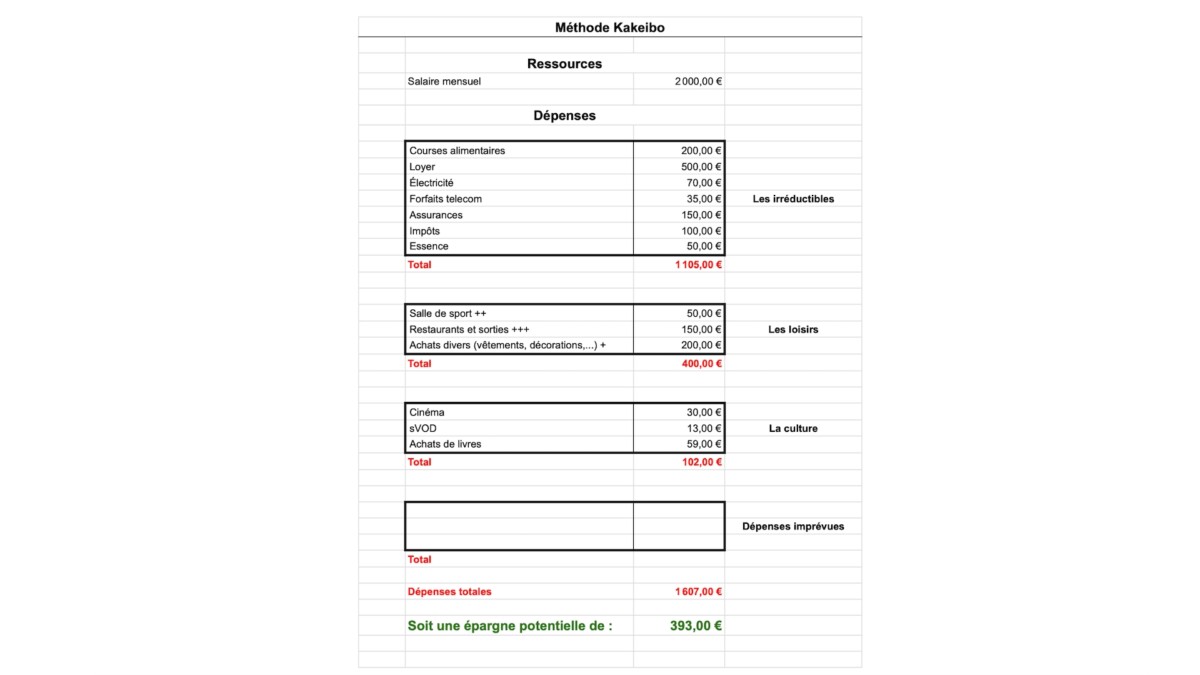

Here is an illustration of a spreadsheet using the Kakeibo method based on 2000 euros of income // Source: Aroged

Here is an illustration of a spreadsheet using the Kakeibo method based on 2000 euros of income // Source: Aroged

First, time for cash flow. Report all of your income, namely salaries, assistance and any additional resources that you receive each month. For the moment, leave aside one-time bonuses if you received them last month.

Next, list all your expenses. To help you, you can create several blocks:

a first for irreducible expenses; a second for leisure activities (note carefully those which give you the most pleasure, Hani Motoko favoring savings of course, but not to the detriment of happiness); a third dedicated to culture (book purchases, sVOD or cinema subscriptions, exhibitions, museums, etc.); a fourth for unforeseen events (for the moment, by definition, this box remains empty).

Now, it's time to add up each category to start to get an idea of the overall breakdown of your monthly budget.

After subtracting your total expenses from your income, you obtain a first estimate of your monthly savings. This will serve as a basis, but the idea is above all to optimize this figure.

And this is where the pleasure weighting comes into play. Perhaps it is possible to limit certain less exciting hobbies, and therefore readjust your monthly savings capacity?

Once this first step is completed, you then have more visibility over the month to come and can begin it with more serenity and organization. But we must not stop there.

Hani Motoko recommends taking stock again at the end of each month, in order to see what worked, the expenses actually reduced and learn from it. The key is to stay in a positive and non-punitive approach, and to regularly find areas of improvement for your budget, and therefore for your future savings.

The 52-week method: the promise of easily reaching 1,400 euros in savings

What if you took inspiration from La Fontaine's fable to put some funds aside? There's no point in running, it's all about time. At the start, no more intense upheavals and indecent amounts of money to save. The 52-week method is intended to be progressive, but no less effective, especially for limited budgets.

Step-by-step you build your savings // Source: Sasun Bughdaryan via Unsplash

Step-by-step you build your savings // Source: Sasun Bughdaryan via Unsplash

The first week, start by isolating 1 euro. Yes, 1 euro, less than the price of a coffee in a vending machine. Then each week, increase this amount by 1 euro, until reaching 52 euros per week at the end of the period. After one year, you will be able to boast of having been able to place 1,378 euros in your Livret A, on your life insurance, or any other risk-free support of your choice.

This solution is above all designed for the most modest and can be modulated as desired depending on your savings capacity. But be careful to estimate week 52 carefully, which could then become unsustainable if from the start you are too ambitious.

The idea is above all to force yourself to put a little aside regularly, without the amount saved becoming an obstacle to your daily life and your essential expenses.

This method can also be used per day. For example, you can start with a symbolic deposit of 1 cent on the first day, then increase daily by one cent, to reach an amount of 3.65 euros on the 365th day. After a year, you will have saved 670 euros. It's a start and nothing stops you from starting at 1.5 cents on the first day of the following year.

Where should the savings thus generated be placed?

These three methods aim above all to generate precautionary savings. In this context, bank books constitute a practical and adequate solution for isolating the funds in your current account, without taking the slightest risk.

But as the Livret A rate is limited to at least 3% until January 2025, it may be appropriate to study the other alternatives available to you. Mon Petit Placement then offers a life insurance contract in euro funds and therefore completely secure: Plan B.

Thanks to the promo code FRANDROID30, Mon Petit Placement offers you the opportunity to discover the service with a 30% discount for one year on fees deducted from your performance.

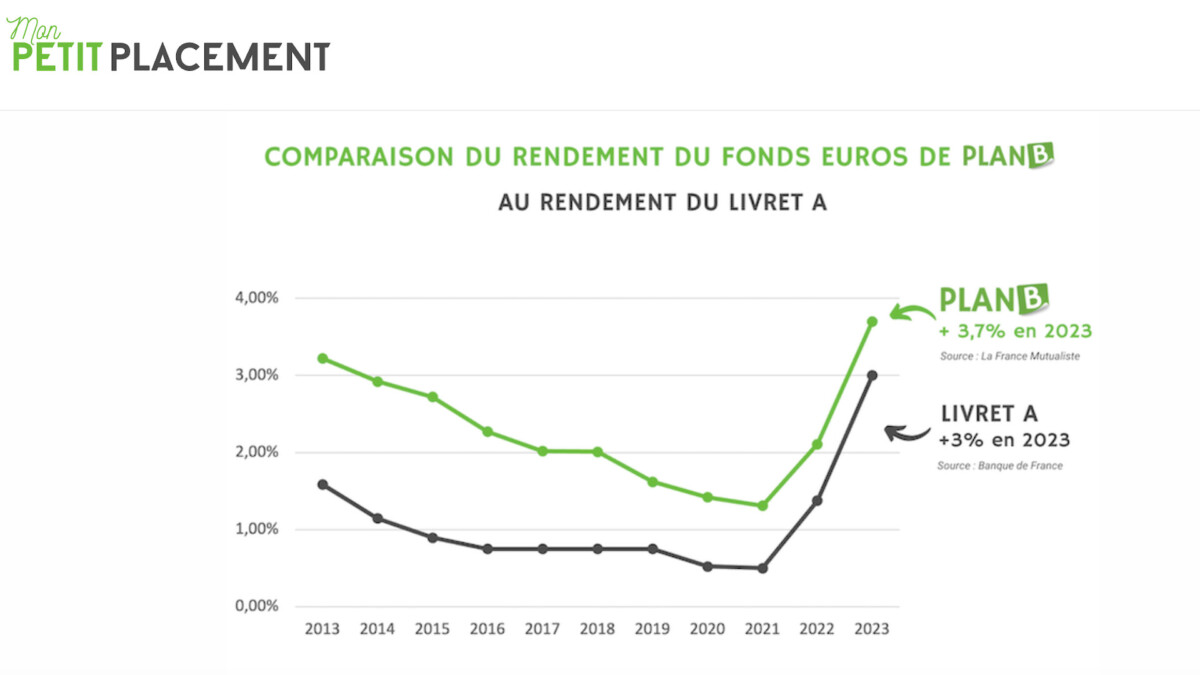

History of returns for Plan B of Mon Petit Placement // Source: Mon Petit Placement

History of returns for Plan B of Mon Petit Placement // Source: Mon Petit Placement

Opting for Plan B means protecting your funds while slightly boosting your savings. In 2023, this investment recorded a rate of return net of management fees of 3.70%, one of the best rates in its category*. This is a great opportunity, especially if you have already reached the limit of your bank accounts. This is without taking into account that if the economy picks up again, you will potentially be able to benefit from the market effect, without risking the slightest loss of capital when it is at half mast.

As a bonus, as with the Livret A, your money is available at any time. In case of need and emergency, you can withdraw all or part of your funds free of charge. This procedure is done in just a few clicks from the Mon Petit Placement application (available on Android and iOS).

Likewise, payments to Plan B are completely free, as are the decisions between the different investment vehicles offered by Mon Petit Placement. Indeed, fintech is not limited to Plan B alone, but has a broader range of life insurance offerings.

Depending on your risk profile and your investment horizon, the French firm allows you to invest in more or less dynamic portfolios** and even to focus on certain specific sectors of activity such as the environment, Tech or still health.

Thanks to the promo code FRANDROID30, Mon Petit Placement offers you the opportunity to discover the service with a 30% discount for one year on fees deducted from your performance.

A simple and quick subscription, but with possible support

Whatever offer you choose, getting started is very simple. Everything happens online from the Mon Petit Placement application or website. All you have to do is create an account, provide your contact details, then answer a quick questionnaire to determine your investor profile.

Then, a personalized investment strategy is sent to you by email. And if necessary, fintech experts are on hand to advise you and answer any questions you may have.

When you're ready, you can sign up for the life insurance of your choice, directly from the app.

* The past returns presented concern the euro fund of the Actagence2 multi-support life insurance contract insured by La France Mutualiste. These returns are given for information only and do not guarantee the future rate of the Euro fund of the Mon Placement Vie contract. Returns are net of management fees and gross of social and tax contributions.

** Unit-linked life insurance represents a risk of capital loss.

{kind=link}